Urea

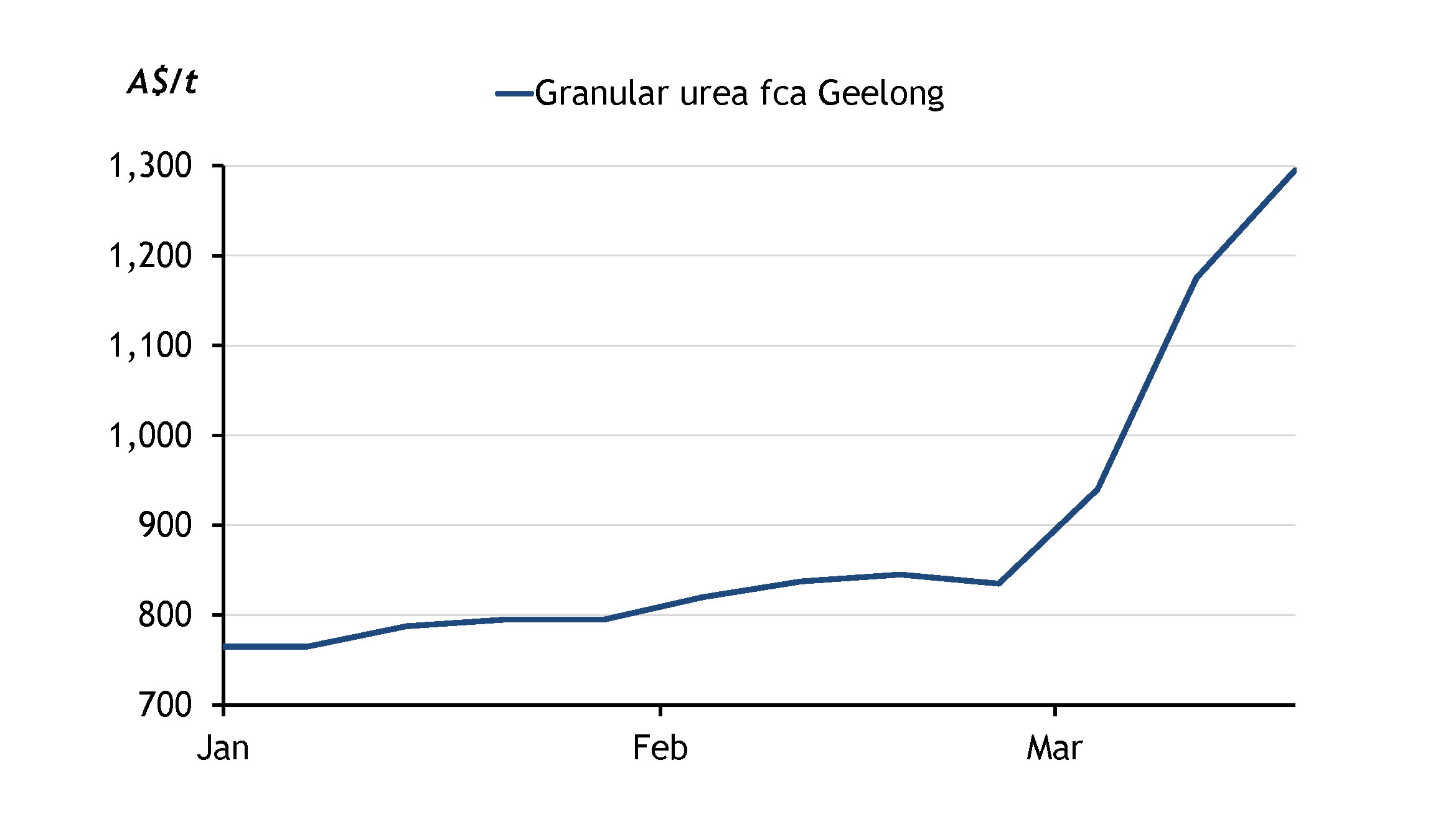

Domestic supply of granular urea remains very tight across Australia and prices continue to rise.

Argus last assessed granular urea at A$1,250-1,340/t fca Geelong on 10 March.

South Australia and Victoria received early Autumn rains, helping to relieve the dry conditions experienced in December and January. South Australia’s key grain growing regions received up to 50mm of rain in the seven days to 18 March after receiving average to very much above average rainfall throughout February, the Australian Bureau of Meteorology data show.

Prompt urea supply is short, but this will not necessarily impact the upcoming pre-seeding fertiliser application as the country is supplied through mid-April, suppliers said. Players in the market are concerned about supply going beyond that, including winter crop top-dressing and summer crop applications.

There are 122,000t of urea in transit across four vessels, equally split between the east and west coast, vessel tracking data from Kpler shows.

Phosphates

Domestic demand for MAP/DAP is quiet, and multiple suppliers are reportedly sold out. Growers and suppliers are more focused on nitrogen products and diesel availability.

There are 394,000t of MAP/DAP and other phosphorous fertilisers in transit to Australia across 11 vessels, Kpler data show.

Australian amsul demand surges on short urea supply

Australian demand for ammonium sulphate (amsul) continues to pick up as the country confronts a sharp tightening in urea availability from the Middle East.

Buying interest for amsul has increased in the past two weeks, as international urea prices soared and supply tightened ahead of the country's peak import demand from April to June. Growers are drawing down amsul stocks in the absence of urea, with affordability further supporting the shift.

Commentary and pricing supplied by Argus Media

Disclaimer: The information provided in this report is general in nature and is intended for informational purposes only.