The Australian Government’s 2026-27 Budget was handed down on Tuesday 12 May 2026.

GrainGrowers welcomed the pre-Budget announcement of the Australian Fuel Security and Resilience package, which addresses several priorities outlined in GrainGrowers' long-standing fuel security policy, and the inclusion of onshore storage for fertiliser stocks. The package includes:

- Government-owned fuel reserve: $3.2 billion investment to establish a 1 billion litre strategic reserve targeted at managing regional stockouts and ensuring supply for essential users.

- Minimum Stockholding Obligation: Increase in offshore, privately held fuel stocks to 50 days of consumption, supported by a $7.5 billion finance facility (which also supports fertiliser security).

- Refining capability support: $10 million in 2026-27 for feasibility studies into new or expanded local fuel refineries.

- Financial support for industry: $1 billion in interest-free loans for manufacturing and logistics businesses to bolster supply chains, delivered through the National Reconstruction Fund.

- Short-term cost relief: Halving the fuel excise and reducing the heavy vehicle road user charge to zero through 30 June 2026.

The Budget demonstrates the Government's commitment to developing a market measure that drives demand for Australian low-carbon liquid fuel production, which GrainGrowers acknowledged is a move in the right direction. GrainGrowers has also welcomed the $8.7 million funding announced for the Australian Pesticides and Veterinary Medicines Authority (APVMA), which is slated to improve efficiencies in the evaluation and approvals processes for agricultural chemicals, supporting agricultural productivity.

However, there are some more contentious Budget measures which GrainGrowers is analysing and working with the National Farmers' Federation (NFF) on advocating improved outcomes for farmers. In particular, a range of tax reform measures were announced: some positive, such as the reintroduction of the loss carry back, making permanent the $20,000 increase to the instant asset write-off for small businesses, and the exemption of primary production income to the new 30 per cent minimum tax on discretionary trusts. Other measures, such as changes to capital gains tax, may impact members.

A summary of these measures is included below, and a detailed analysis of the Budget for the agriculture sector provided by the NFF is available here.

Budget 2026-27: Taxation changes

Source: NFF

In the 2026-27 Federal Budget, the Government announced a suite of changes to Australia’s taxation regime which centred on changes to the Capital Gains Tax (CGT) Discount, Trusts and Negative Gearing. With strong implications for Australian agriculture, this summary of the changes to the CGT Discount and Trusts has been provided by the NFF.

It is important that farmers speak with their finance professional for advice pertaining to individual circumstances. This information is provided only to provide an overview of the tax changes announced in the Budget.

1. Discretionary trusts

The Government is introducing a 30 per cent minimum tax on the taxable income of discretionary trusts from 1 July 2028. The tax will be paid by the trustee; however, beneficiaries in the trust will still need to declare the income in their tax returns but will receive non-refundable credits for the tax payable by the trustee.

- Exclusions: The minimum tax will not apply to primary production income, as well as a range of other types of income (not relevant to this briefing). The minimum tax will not apply to other types of trusts such as fixed and widely held trusts, complying superannuation funds, deceased estates and charitable trusts.

- Rollover relief: Rollover relief will be available to assist small businesses and others that wish to restructure out of a discretionary trust into other arrangements, such as a company or a fixed trust. This will provide expanded relief from income tax consequences, including capital gains tax, for those who choose to restructure, and will be available for three years from 1 July 2027.

2. Capital Gains Tax (CGT) Discount

Existing regime

The CGT discount was introduced in 1999 as part of the Howard Government’s tax reforms following the Ralph Review of Business Taxation. It replaced the earlier system of full indexation for inflation, which had applied since CGT was introduced in 1985, with a flat discount on nominal capital gains of 50 per cent for individuals and trusts and 33.33 per cent for superannuation funds.

The Government argued that a uniform discount would broadly approximate the effect of inflation over time, whilst encouraging investment in the Australian share market, spurring investors to buy and sell assets more frequently and increase tax revenue.

The CGT discount operates whereby when you sell or otherwise dispose of an asset, you can reduce your capital gain by 50 per cent if both of the following apply: you owned the asset for at least 12 months and you are an Australian resident for tax purposes.

The remaining capital gain is then taxed at the taxpayer’s marginal income tax rate.

Example:

James buys a property for $500,000 and sells it 5 years later for $600,000, incurring a $100,000 capital gain. After applying the 50 per cent CGT discount, only $50,000 is added to James’ assessable income, taxed at his personal marginal tax rate, as opposed to the full $100,000.

Proposed changes

The Government is proposing to make the following three primary changes to the CGT regime:

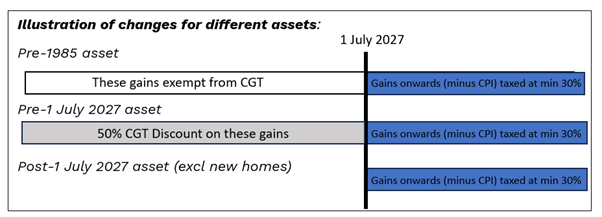

- Removing the 50 per cent CGT discount and returning to the inflation indexation model from 1 July 2027 (with the 50 per cent CGT discount continuing to apply to gains accrued prior to 1 July 2027).

- Introducing a 30 per cent minimum tax on real capital gains (capital gain less inflation) earned from 1 July 2027.

- Bringing pre-1985 assets (which have to date been exempt from paying CGT) into the new inflation indexation model on gains accrued from 1 July 2027 onwards.

Example:

Jane purchases an asset on 1 July 2022 for $800,000. She sells the asset on 1 July 2032 for $1,600,000 earning a 7.2 per cent annual return. Using ATO tools, Jane determines that the asset was worth $1,131,371 at commencement of the policy (1 July 2027).

Under the transitional rules, Jane calculates her taxable capital gain by adding:

- Taxable capital gains of $165,685 earned before commencement, which is equal to gross capital gains of $331,371 with the 50 per cent CGT discount; plus

- Taxable gains of $319,958 earned after commencement, which is equal to the gain of $468,629 less cost base indexation.

Her total taxable capital gain is $485,643. This is more than the $400,000 that would have been calculated if a 50 per cent discount applied to the gain overall. Assuming a 47 per cent tax rate, the tax on her gain is $228,252 (compared to $188,000 with a 50 per cent discount).

2.1 Small business CGT concessions

Alongside the broader CGT reforms introduced in 1999, the Government introduced a suite of small business CGT concessions which allow small businesses to reduce, disregard or defer some or all of a capital gain from an active asset used in a small business. These current small business CGT concessions will continue, unchanged.

To access any of the small business CGT concessions at least one of the following must be met at the time of the CGT event:

- The taxpayer is a small business entity, meaning aggregated annual turnover of less than $2 million; or

- The taxpayer satisfies the maximum net asset value test, meaning the net value of the taxpayer’s CGT assets, plus those of connected entities and affiliates, does not exceed $6 million.

Once the small business eligibility tests are met, there are four small business CGT concessions available that can be layered on top of each other:

- The small business 15-year exemption: The 15‑year exemption is the most generous of the small business CGT concessions and allows an eligible small business owner to completely disregard a capital gain on the sale of a business or business asset. To qualify, the asset must have been owned for at least 15 years, the taxpayer must be 55 or older and retiring (or permanently incapacitated), and the asset must meet the basic small business eligibility conditions.

- The small business 50 per cent active asset reduction: The 50 per cent active asset reduction allows an eligible small business to reduce a capital gain by half if the asset sold is an active asset used in carrying on the business. It applies automatically once the basic small business eligibility conditions are met, unless the taxpayer chooses not to apply it. For individuals and trusts, this reduction can be used in addition to the general 50 per cent CGT discount, meaning that up to 75 per cent of the capital gain can be disregarded before applying any further small business concessions.

- The small business retirement exemption: The small business retirement exemption allows an eligible small business owner to disregard up to $500,000 of capital gains over their lifetime when selling a business or active business asset. If the individual is under 55, the exempt amount must be contributed to a complying superannuation fund or retirement savings account; if they are 55 or over, they can choose to keep the proceeds without a compulsory super contribution. The exemption is designed to help small business owners fund their retirement or exit a business, even where they are not fully retiring at the time of sale.

- The small business roll-over: The small business CGT roll‑over allows an eligible small business to defer all or part of a capital gain arising from the sale of an active business asset, rather than eliminating it outright. The deferred gain is rolled over into a replacement active asset acquired within a specified period (generally from one year before to two years after the CGT event), or it can be temporarily deferred even if no replacement asset is immediately acquired. The roll‑over is intended to support business continuity and reinvestment, with the deferred gain only crystallising if the replacement asset is later disposed of or stops being an active asset.

3. Instant Asset Write Off

As part of the 2026–27 Budget, the Government announced it will permanently increase the instant asset write-off for small businesses to $20,000 from 1 July 2026 to help improve cashflow and reduce compliance costs.

The $20,000 limit under the measure applies on a per asset basis, so small businesses can instantly write off multiple assets.

Under the measure, from 1 July 2026, small businesses with an aggregated turnover of less than $10 million, can deduct:

- The full cost of eligible depreciating assets costing less than $20,000 that are first used or installed ready for use in an income year; and

- An amount included in the second element of an eligible depreciating asset's cost that they have incurred in an income year, if they claimed an immediate deduction for the asset under the simplified depreciation rules in a prior income year where the amount is:

- The first amount of second element cost incurred after the end of the income year in which the asset was written off; and

- Less than $20,000.

4. Loss carry back

As part of the 2026-27 Budget, the Government announced it will reintroduce a permanent loss carry back for tax years commencing on or after 1 July 2026 for companies with an aggregated annual global turnover of less than $1 billion.

The loss carry back will allow companies to carry back a tax revenue loss and offset it against tax paid up to two years earlier. The measure aims to improve cash flow and help firms remain resilient through periods of adjustment or broader economic shocks.

Treasury analysis indicates that when the measure was last used between 2020-21 to 2022-23, the loss carry back provided, on average, a cash flow boost of around $50,000 per business.